This blog is moving on to: https://bluebananaeurope.wordpress.com/

See you there!

The European energy system in perspective: electricity, fuels, and EU's industrial complex

Economically, the European Union (EU) is a giant: it sits at the heart of a geographical space of 80 countries that depend on it for trade and investment, and even align themselves with its currency; moreover, the EU has the world’s largest single market; most multinational companies, therefore, depend on access to the region – which means complying with EU standards. With its regulatory powers, the EU should, therefore, profit widely from globalization. However, overlapping crisis such as the financial turmoil starting in 2008, the refugee crisis of 2015, and Britain’s recent decision to leave the Union, put Europe’s internal coherence into question. Apparently, the national grip on various policy areas remains a weighty obstacle for the pooling of the EU’s ample resources behind common policies.

Hence, the question remains whether the European Union is capable of reaching the internal cohesion necessary to organize Europe’s economic space effectively. To evaluate this question, the concept of geoeconomics in intra-European affairs is an interesting one, as it combines two strands of political theory: First, geoeconomics are based on the complex notion of strong reciprocal intersections between the economic and the political sphere; as a consequence, geoeconomics assumes that (some, not all) governments are guided by weighty companies, while (some) others guide large companies for their own geoeconomic purposes. Second, geoeconomics is rooted in realist IR theory, thus encompassing organized actions by governments to change their external environment in general, or the policies and actions of other states in particular so as to achieve the objectives that have been set by policy makers.

Essentially, geoeconomics, therefore, means states leveraging power via economic means to get other states to do what they would not do otherwise.

This idea of nation-states deploying economic weapons in international power struggles, e.g. productivity, trade balances and foreign investment – is not new. However, throughout the twentieth century the balance of power among nations was typically viewed through the lens of geopolitics, and only recently geoeconomics has (re-) emerged. In (Western-) Europe after 1945 on the other hand, geopolitical thought has been largely replaced by integration theories which see Europe as having developed beyond the anarchy of the international system.

Yet given that the European Union does not represent a fully unified political entity, it is unlikely that geoeconomics, this form of power politics through economic means, is completely contained by the (nevertheless dense) system of supranational institutions on the EU-level. Depending on the specific policy area or section of the Internal Market that are concerned, at least parts of the toolbox of geoeconomic statecraft can therefore be assumed of being available to national policy makers in Europe. And where such instruments are available, it appears rather likely that they are also in use. Geoeconomically motivated statecraft should hence (still) play a (more or less strong) role in the relations between European countries.

Moreover, Member States’ reluctance to transfer powers to supranational bodies is growing, and the EU is increasingly characterized by policy co-ordination between MS (as opposed to deeper Europeanization). In other words, politics on the European level have become somewhat deracinated from the supranationalist dynamics and the legislative framework that characterized supranational governance beyond the nation-state.

Of course entities such as the EU will not being replaced by nation states exerting influence through economic instruments, and neither can Europeanization of politics and business (e.g. lobbying) be ignored. But EU-level policy making can be assumed to happen increasingly under the absence of the Community method, that is based on decision-making logic/procedures characterized by voluntary and informal policy coordination between national governments and national representatives with an increasingly strong national rational.

Open power politics may still be unthinkable in this kind of European framework, but the importance of regional integration as a strategy to gain power by increasing market size and economic opportunities is losing its longstanding attractiveness, while government-company relations are intact on the national level. The decreasing inclination of national governments to govern Europe collectively through the various forms of European governance, should therefore be paralleled with a growing importance of geoeconomics for the behavior of individual EU Members vis-à-vis their neighbors.

The Case of Germany and Poland in the Baltic Energy System – Close Neighbours, Close(r) Cooperation?

International Journal of Energy Economics and Policy, 2016, 6(4), 789-800.

Abstract:

When the Baltic Sea region is included in debates concerning European energy policy, the focus often lies on the transit of natural gas. However, this focus on gas transit is too narrow to fully grasp the region as a wider element within the complex fabric of the European energy system. This article therefore approaches the energy system of the Baltic Sea region in a holistic manner and discusses ows of natural gas, oil, coal, and electricity. Against this backdrop, the article presents and discusses the energy supply and demand situation of the Baltic Sea littoral states. Focussing strictly on the Baltic Sea region in a narrow geographical sense allows a detailed visualisation of energy ows between individual countries. From a geoeconomic perspective, the article then analyses and compares the positions of Germany and Poland in the regional energy system; furthermore, scenarios concerning the effect of Polish and German national energy policies on regional energy flows are presented and discussed. As most European countries are energy importers, this discussion focuses on the effect of national policies on energy imports and their impact on the regional energy system. Based on this discussion, the article evaluates the geoeconomic implications of these scenarios for Poland and Germany and the prospects for better aligning the two countries’ national energy policies.

Lignite mining is boring? Go on a tour to Garzweiler 2 and think again!

Organisation: Thomas Sattich

4 June 2015 from 12:00 – 14:00.

The Chinese government has proposed the New Silk Road, or “one belt and one road”, which would link China and Europe by land and sea. The one belt and one road is a high- level initiative to which the Chinese government attaches enormous importance and would in theory improve interlinkages between China and Europe and the intervening regions. Although the details of the initiative remain unclear, the Chinese government intends that it will an important role in the development of the EU-China economic relationship. Its potential impact in the EU will have many dimensions that are not simply about infrastructure and trade, but also concern key issues such as sustainability.

In the course of the last two decades the concept of a green economy with limited carbon dioxide emissions and reduced resource intensity has evolved to a key element of many European policies. Use of renewables and resource efficient economic and industrial processes are key issues of this sustainability agenda. The integration of two or more economic areas is believed to bring the distribution of resources and markets closer to their optimum. Under certain circumstances the integration of different economies hence appears to be beneficial for EU’s sustainability agenda. Various initiatives of the European Union such as enlargement, neighbourhood policy, trade and investment agreements are based on this assumption.

Accessibility is the key issue in this regard: Without access to markets, no exchange of goods, services and ideas can take place, thus leaving existing patterns of production and consumption unchallenged and unchanged. Economic development is therefore closely tied to network conditions. In other words, existence and state of transport, energy and communication networks determine the capability of putting potential synergies between different regions to practical use. Improving the basis for economic exchange between different regions should therefore present various opportunities for sustainable economic development. The need of cost intensive green technologies for big markets represents only the most prominent example in this regard.

The Chinese government has already committed US$40 billion to a Silk Road infrastructure investment fund. The project would involve not just infrastructure, but will require a broad range of other institutional initiatives such as customs, as well as security. By extension it will also involve Chinese investment in infrastructure in the EU. As a result it is highly likely that China will have a direct impact on the sustainability and integration agendas in the EU. This Policy Forum will address what the impact of the New Silk Road in the EU:

The expert panel will consist of the following panellists:

Chair: Duncan Freeman, Research Fellow, Brussels Institute of Contemporary China Studies

Speakers:

Xiang Yu, First Secretary at the Economic & Commercial Counselor’s office of the Mission of the People’s Republic of China to the European Union

Michael Grabicki, Vice President ZOA BASF Group

Thomas Puls, Senior Economist, Environment, Energy, Transport and Infrastructure, Cologne Institute for Economic Research

We like trains!

The Rape of Europa by Noel-Nicolas Coypel, 1727

At a Mediterranean beach by Nick Hannes, 2013

Authors:

Thomas Sattich

Daniel Scholten, Assistant Professor, Delft University of Technology

Inga Ydersbond, Ph.D fellow/student, University of Oslo

Tor Håkon Inderberg, Senior Research Fellow, Fridtjof Nansen Institute

European Union energy policy calls for nothing less than a profound transformation of the EU’s energy system: by 2050 decarbonised electricity generation with 80-95 per cent fewer greenhouse gas emissions, increased use of renewables, more energy efficiency, a functioning energy market and increased security of supply are to be achieved. Different EU policies (e.g., EU climate and energy package for 2020) are intended to create the political and regulatory framework for this transformation. The sectorial dynamics resulting from these EU policies already affect the systems of electricity generation, transportation and storage in Europe, and the more effective the implementation of new measures the more the structure of Europe’s power system will change in the years to come. Recent initiatives such as the 2030 climate/energy package and the Energy Union are supposed to keep this dynamic up.

Setting new EU targets, however, is not necessarily the same as meeting them. The impact of EU energy policy is likely to have considerable geo-economic implications for individual member states: with increasing market integration come new competitors; coal and gas power plants face new renewable challengers domestically and abroad; and diversification towards new suppliers will result in new trade routes, entry points and infrastructure. Where these implications are at odds with powerful national interests, any member state may point to Article 194, 2 of the Lisbon Treaty and argue that the EU’s energy policy agenda interferes with its given right to determine the conditions for exploiting its energy resources, the choice between different energy sources and the general structure of its energy supply.

The implementation of new policy initiatives therefore involves intense negotiations to conciliate contradicting interests, something that traditionally has been far from easy to achieve. In areas where this process runs into difficulties, the transfer of sovereignty to the European level is usually to be found amongst the suggested solutions. Pooling sovereignty on a new level, however, does not automatically result in a consensus, i.e., conciliate contradicting interests. Rather than focussing on the right level of decision making, European policy makers need to face the (inconvenient truth of) geo-economical frictions within the Union that make it difficult to come to an arrangement. The reminder of this text explains these latter, more structural and sector-related challenges for European energy policy in more detail, and develops some concrete steps towards a political and regulatory framework necessary to overcome them.

Despite some areas with well-integrated power systems (e.g., Scandinavia), European electricity supply still has a largely national (e.g., French), or sub-national (e.g., Bavarian) basis. This, however, does not imply that there is no integration: interconnections exist between most neighbouring countries and regions, and in some of these areas the power transmission infrastructure has significant exchange capacity (e.g., Germany and the Netherlands). In sum, the power system in Europe can be described as a heterogenic patchwork of semi-integrated and non-integrated regional, national and sub-national power systems. Power generation, transmission, distribution and consumption in Europe can thus only partly be described as European.

On various dimensions, EU energy policy aims at breaking the still prevalent national rationale in the energy sector, and at convincing actors that the exchange and trade of electricity within national boundaries is no longer an adequate option. Following these EU policies the system of power generation, transmission and consumption in Europe would take steps towards becoming a European one. The basic assumption behind these policies is that the structure of today’s European power system is sub-optimal and further integration development of the European grid infrastructure is expected to create economies of scale and utilise more of the technical capacity seen from a European level. EU energy policy is therefore expected to result in a more efficient power system with less overcapacity but greater security of supply and lower electricity prices. Moreover, it is widely believed that a deeper integrated system is crucial for the integration of more renewables.

Historically, the involvement of the European Community on the field of energy developed only recently. Due to long investment cycles and permitting processes, and interest structures in the power sectors, the European Union could only partly achieve stronger integration. The Energy Union and the 2030 climate and energy package therefore have to be understood as the latest steps of a continuous effort to accomplish deeper integration of power systems in Europe. The successful implementation of these latest initiatives may, however, run into difficulties, as they – just as earlier initiatives – imply a change in location of generation capacity beyond national borders, thereby altering the topography of the existing power system:

Each of the above-mentioned policies has distinct implications for the power sector of individual member states and thus the geo-economic balance in Europe. To protect their (national) economic assets, each member state will assess the impact of these elements of European energy policy on its national power sector; organised interests within the national energy sector on the other hand will analyse the impact of the three policies on their businesses and start to influence the bargaining position developed by their national governments. Implicitly or explicitly, both sides of the still-existing tight state-company relationships will define a position to be taken in EU-level negotiations towards other European governments and the diverse set of actors on the European level. The resulting frictions at the EU-level would be negligible if the balance between winners and losers was approximately equal across member states, and if the regulatory framework established a level playing field and net gains for all market players; yet, not every country or energy company is likely to benefit equally from the changes involved with new EU policies on the field of energy.

If implemented and effective, EU energy policy may increase dependency on the goodwill and the capability of (power and grid companies in) neighbouring states to uphold electricity supply in another. Europe is hence confronted with a ‘catch-22’: on the one hand are the advantages of European energy policy, but on the other the potentially painful adaptations of power generation, distribution and consumption imply risks for the national (power) industry. Existing or future instruments of EU energy policy will have to overcome reluctance to integrate power systems; where these instruments will be needed, and what form they will have to take, largely depends on variations in member states’ benefits and costs involved with adapting the national energy sector to the ends of EU energy policy.

Taking stock of the various characteristics of national energy systems in Europe is imperative before new EU policies can be negotiated effectively. Moreover, strongly differing political positions on energy-related matters (e.g., renewables, shale gas and nuclear power) between member states need to be identified and systematically analysed. Both the analysis of national energy systems and policies will allow the identification of latent conflicts of interests between member states and options to settle them by means of existing or new instruments of European Union energy policy. Such an analysis of the state of play will ideally help in finding an EU-level energy policy framework capable of overcoming the geo-economic antagonisms that otherwise might constitute a major impediment for the negotiation and/or implementation of new measures and more integration, responding to the questions above. Currently, therefore, three questions need to be addressed:

1.) Which countries, regions and companies are likely to benefit or lose from the energy transition that follows the EU agenda in the field of energy policy, and in what ways?

2.) How will these geo-economic consequences affect patterns of consensus, cooperation and conflict between member states at the European level of energy policy?

3.) Does the European Union have the necessary instruments at its disposal to overcome conflicts of interest, and if not, what instruments could be developed to achieve this?

If policy makers at the European level are to successfully negotiate and implement the Energy Union and the 2030 climate and energy package, they need to find a way to balance the geo-economic frictions between member states caused by EU energy policy. A regulatory framework is needed that is capable of easing geo-economic concerns through transparent governance structures such as co-ownership of grid assets or co-decision making of grid operations, whether between two or more countries or at the EU level. Moreover, at the business level clear contractual agreements between parties regarding energy and cash flows are another means to avoid potential conflict and handle eventualities. Hence, addressing the root causes of conflicting interests is necessary in order to provide institutional means to handle outcomes of EU energy policy that otherwise could be labelled unfair.

The latest developments in the field of EU energy policy do, however, still resemble an eclectic process: the goals are clear, but as of today there is no clearly formulated and fundamental analysis of those geo-economic factors and interests which partly foster, and partly contradict, the implementation of new measures to reach these goals. Issues like the unfinished unbundling process (i.e., of long-established and poorly transparent structures of command and control) or the insecurities surrounding price formation in the renewables sector persist; as a result, the EU’s efforts to stimulate the construction of new (renewable) generation capacity and new interconnectors between member states simultaneously fall short of the possible. Hence, before discussing new EU policies, the will to address those factors that contradict the goals of EU energy policy is imperative. Only then can a fitting framework of measures, instruments and regulations be found that conciliates interests that do not consent.

Thus, in order to reach to reach the goals of EU 2030 and the Energy Union, the will to openly identify and address economic antagonisms caused by EU energy policy is needed. Addressing the three above-mentioned questions is crucial in this regard; however, they have not yet been discussed in full depth by European policy makers and EU-level analysts. In order to come to a binding political agreement, these questions should hence serve as the basis of a systematic and transparent exploration of potential benefits and losses for individual member states resulting from today’s EU energy policy. Only on the basis of such a discussion can the necessary instruments to conciliate various multi-dimensional and more-or-less contradictory private and national interests be identified. Therefore, a high-level group should be initiated that brings together representatives of governments and the energy sector to openly discuss these issues.

Author: Thomas Sattich

Germany’s energy transition changes the demand for energy on regional and international energy markets. A major share of the country’s energy imports comes from, or passes through the Baltic Sea region, making Germany the area’s main energy importer. Public discourse does, however, not reflect this situation accurately. Imports of natural gas block the view on the importance of other energy carriers. The latter, especially oil and coal, are, however, equally important both as elements of the regional energy system and with regard to Germany’s energy future. This article therefore aims at going beyond the narrow focus on natural gas, and provides a more encompassing assessment of the impact Germany’s Energiewende is likely to have on energy flows in the Baltic Sea region.

In 2011 Germany started enthusiastically into its Energiewende adventure. Since then it became clear that the goal of a nuclear free and carbon-neutral energy system is not to be achieved easily or cheaply. The international implications of the project have not received much attention in the beginning; yet in the energy sector things are per definition interrelated and not confined to the national level. Soon after the phase-out of the first eight nuclear power stations, the country hence saw itself confronted with the international dimension of the latest of its energy policy u-turns. But to the major surprise of the general German public, the idea of a quick nuclear phase-out and large-scale increase of renewables did not turn out to be an Exportschlager (export success).

On the contrary, the focus of countries, such as Poland, Sweden and the Great Britain, remained on coal, gas and nuclear power. Others such as Spain even reduced their subsidies for renewables. But even though Germany’s energy transition causes only little enthusiasm in neighbouring countries, the Energiewende still has repercussions in the international energy system: being Europe’s largest importer of energy, the transformation of Germany’s energy system changes demand on international and regional energy markets. Moreover, electricity flows go through the interconnectors between national power systems, and thus have an impact on the emerging EU electricity market. It is thus very likely that the Baltic Sea region will not remain unaffected by the Energiewende.

The aim of this article is a twofold assessment of 1) the role of the Baltic Sea region for Germany’s Energiewende project and 2) the likely impact of this project on energy flows in the region. A short-term and a long-term scenario could serve as the basis for this analysis: according to Germany’s national energy strategy the nuclear phase-out is to be completed by 2022. At this point renewables should contribute with at least 18 per cent to meet national net energy demand, and with at least 35 per cent to electricity demand. By 2050 these renewables are supposed to increase to 60, respectively 80 per cent (BMWi 2014a). As the Energiewende’s history suggests, sudden turns in Germany’s energy policy are possible. As a consequence, the article elaborates on the basis of a 2020/2022 short-term scenario.

What role does the Baltic Sea region play in Germany’s plans to transform its national energy sector? The following section provides an analysis of public discourse in Germany. Aiming at an assessment of those issues that will affect the region’s energy system in the following years, this analysis looks at the Baltic Sea region through the eyes of the country’s energy-interested public. Based on this assessment, the energy system of the region and the likely impact of Germany’s energy system itself is analysed. The focus of this step lies on import/export flows of different energy carriers.

The significance of a particular region for a country’s energy policy should be reflected in the national media coverage: the more important a particular region appears to journalists and experts to be as a source, supply route, and/or location for energy production of a given country, the more prominent its place in the energy related media coverage should be. Similar patterns should be noticeable in the German case. On the basis of this assumption, the following analysis aims at assessing the relative importance of the Baltic Sea region for Germany’s Energiewende. It is based on a sample of 717 articles from five of Germany’s leading daily and weekly newspapers, covering the spectrum from centre-right to centre left and a time period from April 2005[1] to October 2014: Die Zeit (76 articles), Der Spiegel (63), Süddeutsche Zeitung (206), Die Tageszeitung (90), and Die Welt (282).[2]

How much attention does the Baltic Sea region receive in German debates around the Energiewende? From the sample of articles, 134 mention the term ‘Ostsee’ (the Baltic Sea), that is almost 19 per cent. However, this number shrinks drastically if the search term is amended with ‘erneuerbare Energie’ (renewable energy) or ‘Energiewende; only 33 (4.6 per cent), respectively 26 articles (3.6 per cent) discuss the role of the Baltic Sea for the country’s energy transition towards more renewables. In order to put these numbers – and hence the relative importance German press attributes to the Baltic Sea – into perspective, it has to be related to the prominence of other areas. Since Germany is not only a littoral state of the Baltic Sea, it seems logical to ask also about the prominence of the North Sea and other neighbouring regions in German energy-related press (Figure 1).

Based on the findings of this analysis, aforementioned search results appear in a different light. Even though other countries and regions rank higher on the echelons of energy-interested public awareness in Germany, a nevertheless considerable percentage of energy-related press articles seems to discuss the threats or benefits of the Baltic Sea for the country’s energy policy. It can hence be assumed that the Baltic Sea is considered an area of significant importance for Germany’s Energiewende project by German press (and thus the country’s energy-interested public). Moreover, this general interest in the Baltic Sea seems to increase (Figure 2). Yet the results of this analysis are indifferent with regard to the specific role the Baltic Sea plays in energy-related public debates in Germany; the relatively low number of articles in the year 2013, for example, cannot be explained on this basis. In order to provide a better view, a closer look on the specific targets of the Energiewende is necessary.

Figure 1. Percentage of press articles mentioning randomly chosen countries/regions in Germany’s vicinity and renewable energy / Energiewende

Note: ‘Renewable energy’ (outer ring) and ‘Energiewende’ (inner ring).

According to BMWi (2014a, 11), the Energiewende aims at distinctively changing central elements of Germany’s energy system: On the one hand the share of renewables in Germany’s gross energy consumption is to be increased to 18 per cent until 2020 (60 per cent by 2050); on the other hand, the use of primary (fossil and nuclear) energy is to be decreased by 20 per cent (50 per cent by 2050). In sum these and other measures are supposed to decrease green house gas emissions by 40 per cent in the same time period (80 to 95 per cent by 2050). The electricity sector has to play a fundamental role in this programme, with targets even more far reaching: power consumption is to be decreased by 10 per cent until 2020 (25 per cent by 2050), and full nuclear phase-out is to be achieved until 2022. By then (2020) renewables are to increase to a share of 35 per cent in gross final power consumption (80 per cent by 2050).

Figure 2. The varying prominence of the Baltic Sea in German press

Note: Within a sample 134 articles mentioning the Baltic Sea, only a fraction deals with the subject of Germany’s energy transition: Blue line = number of articles mentioning the Baltic Sea (‘Ostsee’) and renewables (‘erneuerbare Energie’); red line = number of articles mentioning the Baltic Sea (‘Ostsee’) and the ‘Energiewende’.

How does German press reflect these targets with regard to the Baltic Sea? While the percentage of newspaper articles from the sample generally reflect the significance of individual Energiewende targets, the Baltic Sea appears to be a blind spot in this regard: only a small fraction of those articles, which are dealing with Energiewende targets also mentions the Baltic Sea. A look at the different forms of energy explains why: German press mostly reflects on the Baltic Sea region with regard to conventional energies; most important in this context is gas and oil, but nuclear energy and coal also play a significant role. Renewable energy, such as solar, biomass and hydropower on the other hand hardly appear at all (Figure 3). The exception that proves the rule in this context is wind power, as more than a third of those articles that mention the Baltic Sea deal with this form of power generation.

In a first approximation this analysis has examined the prominence of the Baltic Sea in German energy-related press; yet the search term ‘Ostsee’ (the Baltic Sea) is too narrow to include the entire region, that is those countries around the Baltic Sea. A deeper assessment therefore has to include the individual littoral states in German Energiewende-related press. There are slight differences between the numbers of articles that mention the search terms ‘Energiewende’, ‘erneuerbare Energie’ and individual countries around the Baltic Sea; yet all in all Poland, Russia, and Sweden appear to be at the centre of attention, whereas Denmark, Finland and Norway attain less attention and rank second in German press.[3] Estonia, Latvia and Lithuania attract the smallest share of attention.

Figure 3. Number of articles mentioning the Baltic Sea and various other types of energy

Note: Within the sample of 134 articles mentioning the Baltic Sea, the prominence of various types of energy varies considerably.

Thus, a few preliminary conclusions can be drawn: if the prominence of the Baltic Sea in German press is taken as an indicator, it appears that the energy-interested public in Germany attributes only limited attention to this region in terms of the Energiewende targets. The interest is, however, growing. Moreover, by broadening the scope to include the littoral states of the Baltic Sea, the picture changes significantly, with individual countries, such as Poland, Russia, and Sweden attaining considerable attention by German press. Seen through the eyes of the German press, the Baltic Sea region is, however, of limited importance with regard to the primary targets of Germany’s energy transition, that is the reduction of (fossil) energy consumption and the increase of renewables. On the contrary, the German press perceives the Baltic Sea region mostly as a supplier for fossil energy, especially gas and oil, or as the location of conventional/nuclear energy based electricity generation capacity.

A closer analysis reinforces this impression: screening the sample of articles mentioning the Baltic Sea for different search terms to appear in the same section as ‘Ostsee’ (the Baltic Sea), almost two thirds of the results account for the term ‘gas’, while only 18 per cent account for ‘wind’. Hence, not only do most articles in the sample largely cover fossil fuels; the particular sections within the articles that contain the search term ‘Ostsee’ also mostly cover the issue of natural gas which is mentioned. The conclusion of this analysis must hence be that gas largely predominates where public discussions in Germany mention the Baltic Sea region and the Energiewende. Given the Energiewende targets to decrease the use of carbon based energy carriers[4], the following sections can hence be based on the hypothesis that – with the exception of wind power – the Baltic Sea region will lose some of its importance for Germany’s energy system.

Where the Baltic Sea region is mentioned, it is largely portrayed as a supplier or supply route for fossil fuels – namely gas – by the German press. In comparison, other forms of energy, such as nuclear energy or biomass, hold an inferior position. The construction of the Nord Stream pipeline might, however, have resulted in a place of gas imports in German public discourse disproportionate to its actual role. Beyond, renewables pose a serious challenge for gas-fired power plants in Germany. The role of natural gas might therefore decrease in the years ahead. The Energiewende targets to generally decrease the use of fossil fuels until 2020 and beyond point in a similar direction. In order to provide a clearer idea of the interactions between Germany’s Energiewende and energy flows in the Baltic Sea, this section will therefore analyse the energy system of the Baltic Sea region in more detail. Basis of this analysis is Eurostat data on energy consumption and imports from 2010-2012 (see Annex).

If the territory of the littoral states is included in the analysis, the Baltic Sea region[5] is an area rich in energy resources, with a three years (2010-2012) average surplus of primary energy production of 500.2 mtoe (million tonnes of oil equivalent). Unsurprisingly, the distribution of available energy resources is, however, highly unequal, with only three countries – Denmark (2010-2012 average surplus of 1.7 mtoe), Norway (2010-2012 average surplus of 169.6 mtoe) and Russia (2010-2012 average surplus of 602.5 mtoe) – showing a positive balance between energy consumption and production. If one compares this (positive or negative) balance with gross energy consumption of individual countries, the seriousness of this situation becomes clearer: with the exception of the three net exporters, the countries of this region do not produce indigenous energy in numbers sufficient to supply the national economies (Figure 4). The energy supply gap of those countries[6] with insufficient access to indigenous energy sources amounts to a (2010-2012) average of -273.7 mtoe.

With an index of -0.613 Germany is to be found amongst those countries that in the region with the smallest basis of indigenous energy. As a result of its internal energy situation and the size of the German economy, the country thus is confronted with a massive (2010-2012 average) energy gap of (-)198.1 mtoe, that is 72.38 per cent of the region’s combined energy supply gaps. 95.3 mtoe – or 48 per cent – of the necessary imports to Germany come from the littoral states of the Baltic Sea littoral.[7] The Baltic Sea region can thus be described as the backbone of Germany’s energy supply, and should be of strategic interest for the country. Given that Germany also accounts for some 24 per cent of gross energy consumption in the Baltic Sea region (including entire Russia), any changes in the German system of energy production, imports and consumption can be expected to affect energy flows in the entire region (Figure 5).

Energy imports from the Russian Federation and Norway play a particular role in this regard, as they account for nearly the totality of imports from the Baltic Sea region to Germany, and hence fill almost half of the country’s energy gap. Including Norway and Russia in the analysis is, however, based on a very broad understanding of the Baltic Sea in terms of geography, as both countries stretch far beyond the geographical limits of that area. This analysis therefore requires a closer definition of the ‘Baltic Sea region’. In this regard it is important to understand that Germany’s national energy system is located at the crossing point of several major Euro-Eurasian energy regions (Högselis, Aberg & Kaijser 2013, 56). German gas and oil imports from Norway, for example, come from fields in the North Sea, and cross that Sea through different pipelines (via Europipe I, Europipe II, and Norpipe); from its entry points to the national German system – located at the shores of the North Sea – Norwegian gas then predominantly supplies areas in North-Western Germany (such as the Ruhr), which, in a more narrow sense, cannot be described as being part of the Baltic Sea region.

Figure 4. Indigenous energy supply of countries in the Baltic Sea region

Note: Red = production of indigenous energy equals national energy consumption; blue = the energy situation of individual countries: negative values = no (use of) indigenous energy (-1) or limited capacity to supply the national economy with indigenous energy; positive values = capacity to fully supply the national economy with indigenous energy plus export capacity (+1 = export equals national consumption)[8].

Source: EUROSTAT online energy statistics (2010-2012), EIA (2010-2012).

In the strict geographical sense, Norwegian gas (2010-2012 average of 25003 mtoe) and oil (8.5 mtoe) supply to Germany can hence mainly be attributed to the North Sea Europe region (Högselis, Aberg & Kaijser 2013, 56); they are thus to be excluded from the following analysis. With energy from Russia, things are more complicated, as parts of the transit system are part of the Baltic energy system (Nord Stream, Yamal/Europol), whereas others (e.g. Brotherhood) pass through different regions. However, yearly transport capacities of individual pipelines[9], and actual gas flows in these pipelines[10] allow to infer an estimated 50 per cent of Russia’s gas and oil supply towards Germany passing through countries in the Baltic Sea region. The following analysis thus includes only those 50 per cent of German oil and gas imports from Russia that can be assumed to pass through the Baltic Sea region.

Figure 5. Who causes, who fills the regional energy gap?

Note: Energy deficit (pink nodes: regional energy deficit, see Annex, Table 2), energy surplus (blue nodes: regional energy surplus, see Annex, Table 2), and energy flows (blue arrows: energy exchange, see Annex, Table 4).[11]. Latvia has not been included in this figure. [12]

Source: EUROSTAT online energy statistics (2010-2012).

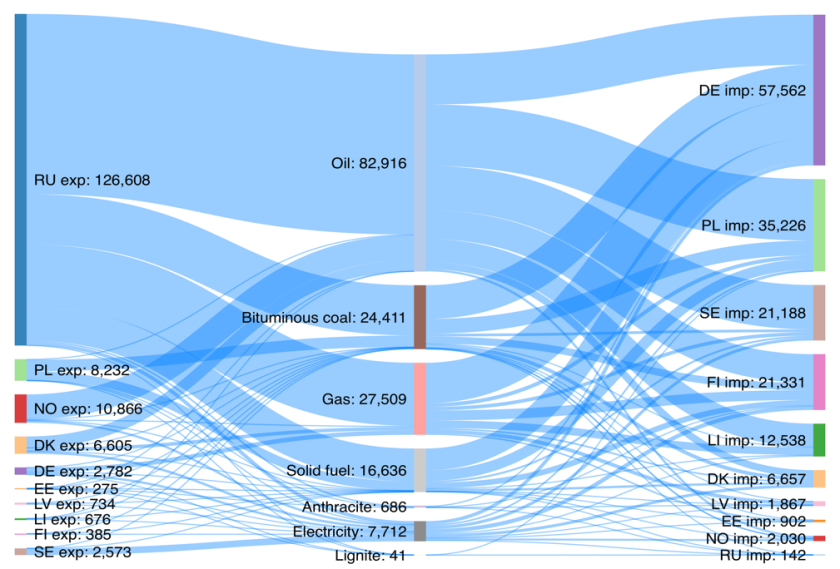

As a result of this, the overall picture of energy flows in the Baltic Sea region changes considerably, and leaves a clearer perspective on the interplay of Germany’s Energiewende with the flux of various forms of energy in the area (Figure 6). Accounting for approximately 79 per cent of energy exports, the predominance of Russia amongst the energy exporting countries remains largely unchallenged in this closer definition of the Baltic Sea region, whereas Norway’s role as energy exporter becomes far less important. Germany’s energy imports from the region reduces largely, to approximately 57.6 mtoe, that is a comparably small 36 per cent share. In other words, the importance of the Baltic Sea region for Germany’s energy sector diminishes if the analysis is based on a strictly geographical understanding of the geographic area.

Moreover, the perspective on different energy carriers as a commodity in the Baltic Sea region changes with an exclusion of Norwegian and Russian sources: while gas is most prominent in the German (Energiewende-related) press on the Baltic Sea region, its actual share amongst those energy carriers which are traded and shipped in the region, is small compared to other energy carriers such as oil and the different forms of coal (see Figure 6). Compared to the flows of oil, gas is only the second most important energy in the energy system of the region, and depending on the share of coal among solid fuels[13] it is likely that gas even ranks third. An analysis of the impact of Germany’s Energiewende on energy flows in the region has to take this limited role of gas into account. Moreover, the place of electricity imports and exports in the region amongst other forms of energy flows has to be noted, as its relatively small share indicates that electricity generation still has a very strong national basis.

Figure 6. Energy flows in the Baltic Sea region[14]

Note: Energy export and import patterns in the Baltic Sea region (2010-2012 average, in ktoe).

Source: EUROSTAT online energy statistics (2010-2012).

Its scarcity of indigenous energy resources makes Germany irrelevant as an energy exporter.[15] Regardless of major modifications of Germany’s energy system, such as the Energiewende, this is unlikely to change. As an importer Germany plays, however, an important role in different energy markets. With a yearly average of 57.6 mtoe (2010-2012) of energy imports, 25 per cent of Germany’s total imports of 176.4 mtoe (2010-2012 average) come from or pass through the Baltic Sea region.[16] To put it differently, 36 per cent of the Baltic Sea region’s total energy flows enter Germany’s energy system. The Energiewende will affect this pattern (until 2020 and beyond), yet the question is, how and to what extent. Since Germany’s exports is unlikely to change significantly[17], the reminder of this section focuses on energy imports.

Based on an energy scenario from 2010 (Prognos, EWI, GWS 2010)[18], it can be assumed that Germany’s energy imports from the Baltic Sea region will decrease by 27 per cent to 41.8 mtoe until the year 2020 (Figure 7). In today’s numbers, this implies that Germany remains the largest destination for energy flows within the region, but the country’s share of imports would reduce from 36 to 26 per cent. As a consequence, the region’s combined energy deficit of -273.7 mtoe (see Annex, Table 2) would be reduced by about 15 per cent. In other words, energy demand would decrease. Yet in order to infer from Germany’s national energy policy on future energy flows in the entire region, several factors need to be taken into account, namely economic growth, national policies of neighbouring countries, and energy prices.

Sound and continuing economic growth of Germany’s eastern neighbours, makes it, for example, possible that by 2020 Poland will be the region’s main importer of energy from the Baltic Sea region.[19] In view of relatively large share of oil, development of road traffic and transport could be a decisive factor in this regard, both in Germany and other countries. National policies are very different in terms of their approach to road traffic: while Germany implemented programmes to promote the use of electric cars and increase their number from only 12,156 at the beginning of 2014 (Car Sales Statistics 2014) to one million by 2020 (Bundesregierung n.d.), other countries did not. Depending on the success of Germany’s policy to convince consumers of the benefits of electric cars, oil demand will develop accordingly.

Figure 7. Energy imports of Germany (in mtoe, average 2010-2012, import scenario 2020)

Sources: EUROSTAT online energy statistics (2010-2012) and Prognos, EWI, GWS (2010).

Other national policies, such as supply diversification programmes in Poland and the Baltic States – that is increased use of LNG from overseas and of indigenous shale gas, as well as the continued use of nuclear power (in Sweden and Finland) and/or the successful construction of new nuclear plants and the necessary grid infrastructure (in Poland and the Baltic States) – might generally reduce demand for gas in the region (largely gas from Russia). Whether Germany will actually retain its role as the region’s main importer thus depends on the development of German demand for natural gas, bituminous coal, and solid fuels. Their place in Germany’s energy system is, however, very much unclear. The reason behind this uncertainty is to be found at the very core of Germany’s Energiewende project – namely the phase-out of plants suitable for meeting base load requirements and increasing number of intermittent renewables.

Both technically and economically this combination of decreasing numbers of base-load generators and increasing numbers of peaking units such as solar and wind power is a complex issue, and – despite many scenarios and plans – there is no blueprint for a system where decentralised and intermittent renewables largely replace centralised base load plants. Flexible gas and biomass power plants are seen as the ideal technological link between the two elements; yet as the case of Europe’s most recent gas power plant in Irsching (FAZ, 2015)[20], illustrates, investments in state-of-the-art equipment and turbines becomes unprofitable under the economic conditions of the Energiewende: as renewables have priority access to the grid, are growing in numbers, and come with low prices at peak hours, there market for gas and other fossil fuels is shrinking, reduced to periods of little wind and sun. Moreover, gas faces a double challenge, as coal still outcompetes gas due to lower prices.

The development of Germany’s gas imports hence largely depends on the question whether policy makers agree on a capacity market that provides an economic framework suitable to keep gas plants in the system. Such a step is currently under discussion (BMWi, 2014b). Outcomes of this discussion and their implementation will certainly affect Germany’s demand for coal and gas imports. Notwithstanding the results of this political process, the demand for biomass is likely to increase in Germany over the following years, because this form of energy – either used in decentralised plants or in form of co-combustion in existing fossil fuel plants.[21] The share of biomass amongst energy imports is thus to until 2020. Depending on the availability of biomass and the outcomes of Germany debates on capacity markets, this energy source is hence – to a larger or smaller extent – to replace either coal or gas in Germany’s energy imports from the Baltic Sea region.

Against the backdrop of energy imports and exports patterns in Northeast Europe, this article analyses the place of the Baltic Sea region in Germany’s public discussions about the country’s energy future; natural gas imports from Norway and Russia largely dominate this public discourse. The construction of the Nord Stream pipeline is likely to be one of the reason for this highly topical nature of gas in German public discourse; it can hence be assumed that the perception of the Baltic Sea region by the German public is largely distorted. This article therefore attempts to broaden the discussion by expanding the focus of the analysis to include other forms of energy such as coal and electricity. On the other hand, this article attempts to focus on the energy system of the Baltic Sea region in the narrower sense. As Norwegian oil and gas exports to Germany come from and through the North Sea, they are hence excluded from this analysis. And as about half of Russia’s oil and gas exports to Germany pass through Central Europe, they are equally excluded.

The result of this analysis is, that the importance of the Baltic Sea region for the future of Germany’s energy supply is not fully grasped by German public. Individual countries such as Poland and Russia obtain varying degrees of attention, and so do the various forms of energy. But all in all the narrow focus on gas largely hides the role of other forms of energy coming to Germany from or through the Baltic Sea region, and thus the true role of the area for Germany’s future energy system. Taking the bigger picture of energy flows in the Baltic Sea region into account, the role of gas imports from Russia appears overestimated in German discussions concerning the role of the Baltic Sea region for Germany’s energy supply: even though Russia is the region’s main supplier of energy, natural gas is not the most important energy carrier. The focus of German media on this topic hence seems to obstruct the view on other important energy carriers, such as coal and – most importantly – oil, which are at least equally important.

As a response to the growing role of renewables, Germany currently discusses a new market design for fossil fuel power stations. Capacity markets for coal and gas-fired plants will be the likely result of these debates, as backup for the notoriously volatile renewables is needed. As Germany is the region’s largest importer of gas and coal, the design of these markets will largely determine the impact of Germany’s Energiewende on regional flows. The way Germany’s Energiewende will affect patterns of energy exports and imports in the region depends, however, on more factors. The future of the German transport sector will at least be equally important, as oil represents the largest share in energy flows in the region. Widespread use of electric cars could serve as a storage battery for intermittent wind and solar power; in 2014 the German government therefore renewed its support with a broad range of incentives for the use of electric cars.

It remains, however, to be seen whether the customers of the German car industry see electric cars as an attractive option. If they do, Germany’s role as an importer of energy from the Baltic Sea region could diminish largely. In this case, Germany’s place in the energy system of the Baltic Sea region will be determined by the results of current discussions about a capacity market for flexible fossil power stations. Depending on the exact outcomes of these debates, German energy imports could decrease according to official scenarios. In such a case, Germany might lose its role as the region’s main importer of energy. For those countries in the region which have only limited access to indigenous energy resources and hence can only play a minor role in supplying Germany’s energy system, such a development is not necessarily a bad one, as their bargaining position on the regional energy market would improve, especially if they successfully implement programmes to further diversify their energy supply.

Auer J. and Anatolitis V. (2014) The changing energy mix in Germany. The drivers are the Energiewende and international trends. Deutsche Bank Research. Current Issues, June 26, 2014.

BMWi (2014a) Zweiter Monitoring-Bericht „Energie der Zukunft“. Berlin: Bundesministerium für Wirtschaft und Energie BMWi.

BMWi (2014b) An Electricity Market for Germany’s Energy Transition. Discussion Paper oft he Federal Ministry for Economic Affairs and Energy (Green Paper). Berlin: Bundesministerium für Wirtschaft und Energie BMWi.

Bundesregierung (n.d.) Leitmarkt und Leitanbieter für Elektromobilität. Retrieved from http://www.bundesregierung.de/Webs/Breg/DE/Themen/Energiewende/Mobilitaet/podcast/_node.html, date accessed: April 9, 2014.

Car Sales Statistics (2014) 2014 Germany: Total Number of Electric Cars, March 29, 2014. Retrieved from http://www.best-selling-cars.com/germany/2014-germany-total-number-electric-cars/, date accessed: April 9, 2014.

CIEP (n.d.) Russian Gas Imports to Europe and Security of Supply. Fact Sheet. The Hague: Clingendael International Energy Programme.

EIA online energy statistics (2010-2012), annual import of different forms of energy.

EUROSTAT online energy statistics (2010-2012), annual import of different forms of energy.

FAZ (2015) Energiewende. Irrsinn in Herrsching. Frankfurter Allgemeine Zeitung, March 17, 2015.

Gazprom Export (2015) Transportation. Retrieved from http://www.gazpromexport.ru/en/projects/transportation/, date accessed: February 11, 2015.

Högselis P., Aberg A. and Kaijser A. (2013) Natural Gas in Cold War Europe: The Making of a Critical Infrastructure. In The Making of Europe’s Critical Infrastructure. Common Connections and Shared Vulnerabilities, edited by Per Högselius, Anique Hommels, Arne Kaijser, Erik van der Vleuten, 2761-101. Basingstoke: Palgrave Macmillan.

OECD and IEA (2004) Energy Statistics Manual. Paris: Organisation for Economic Co-operation and development, International Energy Agency.

Prognos, EWI and GWS (2010) Energieszenarien für ein Energiekonzept der Bundesregierung. Studie für das Bundesministerium für Wirtschaft und Technologie. Basel, Köln, Osnabrück: Prognos AG, Energiewirtschaftliches Institut an der Universität zu Köln, Gesellschaft für Wirtschaftliche Strukturforschung mbH.

Sattich T. (2014) Germany’s Energy Transition and the European Electricity Market. Journal of Energy and Power Engineering, 8(2): 264-273.

Table 1. Yearly energy production and consumption in the Baltic Sea region (2010-2012 average, in ktoe)

| Country | Average consumption | Average production | Balance |

| DE | 322773.17 | 124684.17 | -198089 |

| DK | 18875.73 | 20578.53 | 1702.8 |

| EE | 6149.33 | 5019.9 | -1129.43 |

| FI | 35892.37 | 17173.87 | -18718.5 |

| LI | 6963.77 | 1306.27 | -5657.5 |

| LV | 4514.33 | 2129.7 | -2384.63 |

| NO | 30346.63 | 199960.77 | 169614.13 |

| PL | 99841.07 | 68491.9 | -31349.17 |

| RU | 772254 | 1374802.8 | 602548.8 |

| SE | 50100.53 | 33757.9 | -16342.63 |

Table 2. Yearly energy deficit/surplus in the Baltic Sea region (2010-2012 average, in ktoe)

| Country | In per cent of national consumption | In per cent of regional deficit

(-273670.87 ktoe) |

In per cent of regional surplus

(773865.73 ktoe) |

| DE | -61.37 | -72.38 | |

| DK | +9.02 | 0.2 | |

| EE | -18.37 | -0.41 | |

| FI | -52.15 | -6.84 | |

| LI | -81.24 | -2.07 | |

| LV | -52.82 | -0.87 | |

| NO | +558.92 | 21.9 | |

| PL | -31.4 | -11.45 | |

| RU | +78.02 | 77.9 | |

| SE | -32.62 | -5.97 |

Table 3. Exchange of energy in the Baltic Sea region (2010-2012 average, in ktoe)[22]

| DE | DK | EE | FI | LI | LV | NO | PL | RU | SE | |

| DE | 0 | 539.7 | 0 | 0 | 0 | 0 | 0 | 1764.1 | 0 | 90.2 |

| DK | 1760.1 | 0 | 0 | 0 | 0 | 0 | 204.8 | 28.1 | 0 | 4421.4 |

| EE | 0 | 0 | 0 | 114.4 | 0 | 249 | 0 | 0 | 0 | 0 |

| FI | 68.1 | 0 | 0 | 0 | 0 | 0 | 10.7 | 0 | 0 | 218.4 |

| LI | 88.7 | 0 | 0 | 0 | 0 | 27.8 | 0 | 0 | 0 | 0 |

| LV | 0 | 0 | 89.53 | 0 | 258.4 | 0 | 0 | 0 | 0 | 0 |

| NO | 30943.6 | 3228.1 | 0 | 988.3 | 0 | 0 | 0 | 1114.9 | 0 | 5265.5 |

| PL | 222.6 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 25.8 |

| RU | 62056.0 | 84.1 | 537.0 | 14067.2 | 3542.2[23] | 0 | 828.2 | 21846.2 | 0 | 8959.0 |

| SE | 173 | 489.5 | 0 | 611.7 | 0 | 0 | 521.8 | 141.8 | 0 | 0 |

Table 4. Exchange of energy in the Baltic Sea region (2010-2012 average, in per cent of regional deficit[24])[25]

| DE | DK | EE | FI | LI | LV | NO | PL | RU | SE | |

| DE | 0 | 0.2 | 0 | 0 | 0 | 0 | 0 | 0.64 | 0 | 0.03 |

| DK | 0.6 | 0 | 0 | 0 | 0 | 0 | 0.07 | 0.01 | 0 | 1.6 |

| EE | 0 | 0 | 0 | 0.04 | 0 | 0.09 | 0 | 0 | 0 | 0 |

| FI | 0.02 | 0 | 0 | 0 | 0 | 0 | 0.004 | 0 | 0 | 0.08 |

| LI | 0.03 | 0 | 0 | 0 | 0 | 0.01 | 0 | 0 | 0 | 0 |

| LV | 0 | 0 | 0.03 | 0 | 0.09 | 0 | 0 | 0 | 0 | 0 |

| NO | 11.3 | 1.2 | 0 | 0.4 | 0 | 0 | 0 | 0.4 | 0 | 1.9 |

| PL | 0.08 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.009 |

| RU | 22.7 | 0.03 | 0.2 | 5.1 | 1.3 | 0 | 0.3 | 8 | 0 | 3.3 |

| SE | 0.06 | 0.2 | 0 | 0.2 | 0 | 0 | 1.9 | 0.05 | 0 | 0 |

Table 5. Exchange of energy in the Baltic Sea region (2010-2012 average, in % of national deficit of importing countries, see Table 1)[26]

| DE | DK | EE | FI | LI | LV | NO | PL | RU | SE | |

| DE | 0 | n/a | 0 | 0 | 0 | 0 | n/a | 5.63 | n/a | 0.55 |

| DK | 0.89 | n/a | 0 | 0 | 0 | 0 | n/a | 0.09 | n/a | 27.05 |

| EE | 0 | n/a | 0 | 0.61 | 0 | 10.44 | n/a | 0 | n/a | 0 |

| FI | 0.03 | n/a | 0 | 0 | 0 | 0 | n/a | 0 | n/a | 1.34 |

| LI | 0.04 | n/a | 0 | 0 | 0 | 1.17 | n/a | 0 | n/a | 0 |

| LV | 0 | n/a | 7.93 | 0 | 4.57 | 0 | n/a | 0 | n/a | 0 |

| NO | 15.6 | n/a | 0 | 5.28 | 0 | 0 | n/a | 3.56 | n/a | 32.22 |

| PL | 0.11 | n/a | 0 | 0 | 0 | 0 | n/a | 0 | n/a | 0.16 |

| RU | 31.33 | n/a | 47.55 | 75.15 | 62.61 | 0 | n/a | 69.69 | n/a | 54.82 |

| SE | 0.08 | n/a | 0 | 3.27 | 0 | 0 | n/a | 0.45 | n/a | 0 |

[1] The first Merkel Cabinet was formed in November 2005.

[2] These articles have been retrieved from the Factiva data base, using a number of energy-related search terms in various combinations. Search Terms used in Factiva data base: Nord Stream, Energiesicherheit (energy security), Ostseepipeline (Baltic Sea pipeline), Ostsee-pipeline, Nord Stream-pipeline, Nord Stream pipeline, Erneuerbare Energien (renewable energies), Energiewende (energy transition), Regenerative Energien (renewable energies), Alternative Energien (alternative energies), Energieunabhängigkeit (energy independence), Gaslieferung (gas supply), Energieknappheit (energy scarcity), Blackout, Atomenergie (atomic energy), Kernenergie (nuclear energy), Nuklearenergie (nuclear energy), Energiesicherheit (energy security), Grenzüberschreitende Stromflüsse (cross-border power flows), Elektrizität (electricity), Strom (power), Phasenschieber (phase shifter), deutscher Strom (German power), grenzüberschreitende Leitung (cross-border power line), Atomkraftwerk (atomic power station), Atommüll (atomic waste), Atommüllendlager (nuclear waste disposal facility), Atomendlager (nuclear waste repository), Schiefergas (shale gas), Unkonventionelles Gas (unconventional gas), Shale Gas, Fracking. A full list of word combinations can be obtained from the author.

[3] Number of articles mentioning ‘Energiewende’ is as follows: Poland (41), Russia (36), Sweden (9), Norway (9), Denmark (8), Finland (6), Estonia (4), Lithuania (1) and Latvia (0). Number of articles mentioning ‘Erneuerbare Energie’ (renewable energy) is as follows: Russia (45), Poland (37), Sweden (20), Finland (14), Norway (12), Denmark (6), Estonia (3), Lithuania (1), and Latvia (0).

[4] Accordingly the need for CO2 neutral prime energy carriers will increase.

[5] In this analysis the following countries are included: DE (Germany), DK (Denmark), EE (Estonia), FI (Finland), LI (Lithuania), LV (Latvia), NO (Norway), PL (Poland), SE (Sweden), and RU (Russia).

[6] Estonia, Finland, Germany, Latvia, Lithuania, Poland and Sweden.

[7] German energy imports from the Baltic Sea region (in per cent): RU: 31.33; NO: 15.6; DK: 0.89; FI: 0.03; LI: 0.04; PL: 0.11; SE: 0.08.

[8] Norway has an index value of 5.6.

[9] The annual pipeline capacities are as follows: Brotherhood 100 bcm/year; Yamal 33 bcm/year; and Nord Stream 55 bcm/year (Gazprom 2015).

[10] In 2013, gas flows were as follows: Brotherhood 59 bcm; Yamal 34 bcm; and Nord Stream 23.5 bcm (see CIEP n.d.).

[11] Computed with Gephi, ForceAtlas2.

[12] According to Eurostat data, Latvia did not import energy from the region’s main energy suppliers in the time period 2010-2012.

[13] Eurostat does not provide a clear definition of the term ‘solid fuel’ (for a definition, see OECD and IEA 2004, 109).

[14] For the calorific values used for the conversion of Eurostat data on different forms of energy to ktoe; Anthracite 35 MJ/kg; Bituminous coal 29.5 MJ/kg; Lignite 17.5 MJ/kg; and Solid fuel 20.65 MJ/kg (OECD and IEA 2004, 109).

[15] In view of the decision to phase-out economic support for hard coal mining until 2018 (Auer and Anatolitis, 2014, 7), it is even more likely that Germany’s limited role as an exporter will not change.

[16] Note that 100 per cent of oil and gas imports from Norway, and 50 per cent of oil and gas imports from Russia have been excluded from this analysis.

[17] Electricity may become the exception to this rule, as the increased recourse on electricity generation from renewable sources might exacerbate network fluctuations (see Sattich 2014).

[18] The following analysis is based on the average of individual scenarios to be found in Prognos, EWI and GWS 2010 (note: the reference scenario is not included).

[19] Based on a hypothetical yearly growth rate of three per cent, Poland’s energy imports from the Baltic Sea region could increase to a hypothetical 40.5 mtoe.

[20] This ultramodern gas-fired power plant, equipped with a most advanced and efficient turbine from Siemens might be forced out of business by heavy price competition from solar power.

[21] EUROSTAT provides no precise definition of the term solid fuel; the data does hence not allow to determine the share of biomass within this category.

[22] EUROSTAT online energy statistics (2010-2012); exporters: left column, importers: top line.

[23] According to Eurostat data, Lithuania imported 11661.9 ktoe of energy from Russia. Given that Lithuania has an average yearly energy consumption of 6963.77 ktoe, this figure appears to contain energy transfers to Russia’s Kaliningrad enclave. According to IEA data, Lithuania exported 8119.66 ktoe to Russia. It can hence be assumed that net energy export of Russia to Lithuania amounts to 3542.24 ktoe.

[24] -273670.87 ktoe

[25] See footnote 21.

[26] EUROSTAT online energy statistics (2010-2012); exporters: left column, importers: top line (in per cent of national energy supply gap); Table shows energy exports (Table 3)/national energy balance (Table 1).